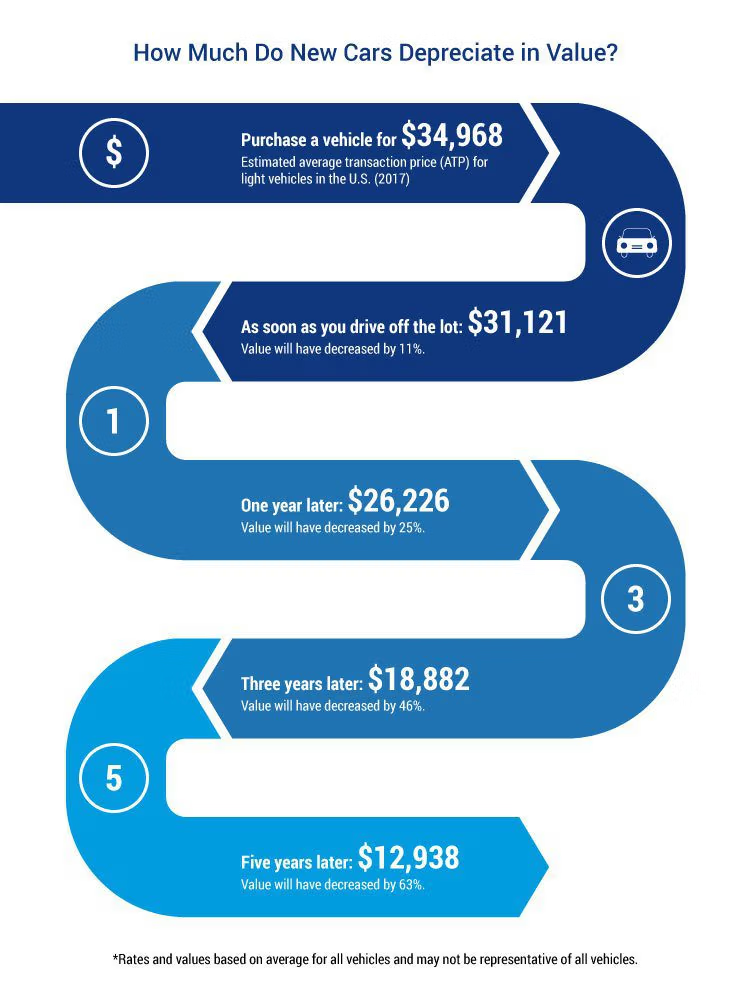

When buying a car, in Hamilton Ontario included, you have to be prepared to lose money… Over time. No one wants to throw money away, and whether or not you will do that with a car purchase is up to you and your negotiation skills and the amount of preparation you’ve invested before buying a car. But one thing is for sure – cars tend to lose value as time goes by and start as soon as you drive them off the dealer’s parking lot.

New cars usually lose around 11% in value as soon as you take them off the dealer’s lot, and by the end of the first year of driving, their value has decreased by 25%. However, the good news is that after that first year, the vehicle will lose its value more slowly but will depreciate nevertheless. The average depreciation rate in the first 5 years is between 15% and 25% per year.

However, the problem arises when you have NEGATIVE EQUITY – when your car is worth less than the amount you owe on your car loan.

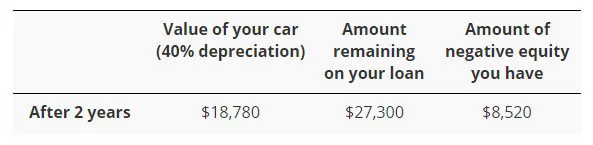

For example, if you bought a new car at a purchase price of $31,300 (plus taxes and fees cost an additional $3,700), you paid for the car with a $35,000 car loan with an interest rate of 4% for an 8-year term. With a depreciation rate of 40%, your car would be worth $8,520 less than what you owe on your car loan.

However, it’s important to underline that the longer loan term makes it harder to get out of a negative equity situation.

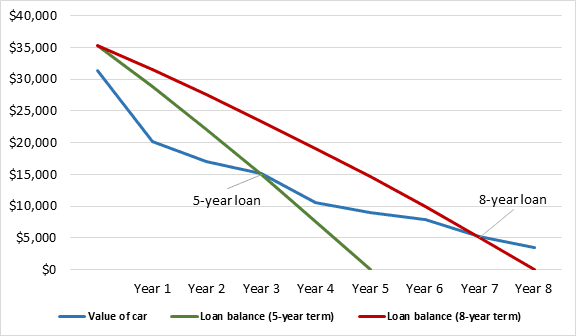

A comparison of negative equity situations on a $31,300 car with a 4% interest rate gives different results if the car loan is for 5 years and if it’s for an 8-year period. With a 5-year loan, you would begin accumulating POSITIVE EQUITY (when your car is worth more than what you owe on your car loan) towards the end of the 4th year. By contrast, with an 8-year loan, you would be in a negative equity situation up until the 7th year of your loan. Moreover, NEGATIVE EQUITY tends to be higher in the first 2 years of a car loan because cars depreciate quickly in the first year of use. Remember, a larger portion of your regular loan payments goes towards interest in the first few years.

There are some financial risks of negative equity:

1) Selling: If something unexpected happens and you need to sell your car quickly, you may lose money. If your car is worth less than the amount you owe on your loan, you might have to borrow money to cover the difference between what you can sell your car for and what you still owe.

2) Accidents: If you get into an accident and your car is a total loss, the money you get from the insurance company may not cover what you still owe on your car loan unless you have extra insurance coverage. For example, if your insurance company decides the replacement value of your car is $10,000, but you still owe $16,000 on your loan, you will need to cover the $6,000 shortfall.

3) Trade-ins: If your car is worth less than the amount you owe on your loan and you trade in your car at a dealership to buy another, you may pay a lot of extra money. You might need to borrow to pay for the new car and cover the amount still owing on the old loan, which could add up to a larger loan and more interest charges. In turn, this could result in even more negative equity.

However, not all car models depreciate equally quickly:

1) Gas Guzzlers: Vehicles with lower MPG tend to fall out of contention due to the extra cost and guilt.

2) Luxury: Cars built for showing off tend to lose most of their shine within the first few years.

3) Longevity: Cars not known for their reliability tend to depreciate quickly.

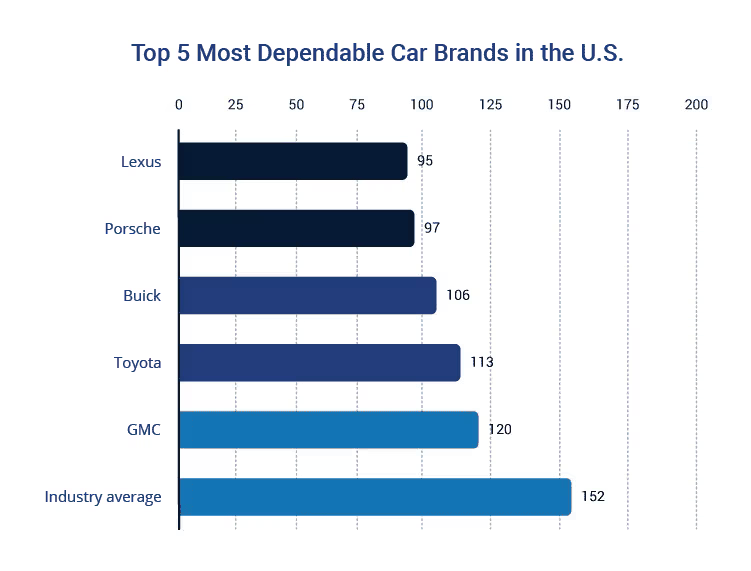

According to TrustedChoice, the most dependable car brands in the US (and Canada is not far off) are Lexus, Porsche, Buick, Toyota and GMC.

Therefore, there ARE ways to limit the total depreciation you can implement yourself – you cannot stop it altogether, but you can slow it down:

Buy a used car (3-5 years old): Let the previous owner eat the depreciation.

2) Wait: Once a car hits 10 years, depreciation is no longer a factor.

3) Maintain the value: Keep your service records up-to-date and repair any damage quickly.

4) Buy smartly: Choose a popular colour and options that will add value to your car if/once you sell it.

5) Low mileage: Keep your miles down as much as you can to help increase resale value.

Current State of Vehicle Depreciation

How much money do you lose buying a new car in the current market? According to the Canadian Black Book – Fitch Ratings “Vehicle Depreciation Report 2022”, cars and trucks have historically been depreciating assets, as we know. But in 2021, that changed due to the impact of global events. The unavailability of new vehicles increased the value of used vehicles, and it continued into the current year. The car depreciation chart (p.6) shows that in 2019, depreciation of used vehicles in Canada stood at -12.6%, but in 2021 it appreciated to 18.9%, although the value is expected to decrease once again in 2022 to -6.1%. What caused the appreciation?

- Ongoing supply chain issues limited the availability of new vehicles

- Increased exports of Canadian used vehicles to the USA

- Limited availability of de-fleeted rental company vehicles

- High post-recession demand for new and used vehicles.

Depreciation of Electric Vehicles (EVs)

According to the Government of Canada, transportation is responsible for 25% of Canada’s greenhouse gas emissions (GHG), of which almost half comes from light trucks and passenger cars. To shift to cleaner fuels, they set a mandatory target for all new light-duty cars and passenger trucks to be zero-emission by 2035. Consequently, there will be more Electric Vehicles (EVs) on the roads in future, but do they depreciate in the same way as cars with an internal combustion engine (ICE)?

Battery electric vehicles (BEVs) have few parts compared to a standard gasoline-driven car. In the Black Book depreciation report, they maintain that assuming electric vehicles will last longer is not necessarily correct. They feel that due to various factors, there is no significant difference in the expected life span and average car depreciation rate of gas and electric vehicles.

Use Quality Auto Repair Services in Hamilton To Limit Depreciation

CRS Automotive Services Hamilton might not have the latest car depreciation chart by model, nor are we able to assist when you wonder how much new cars depreciate. Still, we can help you with quality auto repair services. It will contribute to maintaining your car’s value and keeping your loved ones safe. What can we do for you?

Brake repair services: Front and rear brake pad inspection, brake fluid change, parking brake repair, brake pad installation, emergency brake repair.

Tire repair services: Tire rotation, balancing, rim repairs, flat tire repairs.

Oil change services: Inspecting oil filter, air filter, vehicle lubrication, transmission filter, antifreeze coolant, and engine coolant.

Suspension repair services: Inspect suspension when clients experience braking problems, odd noises, and uncontrolled bouncing when driving.

A/C and Heating service: Inspecting refrigerant leaks and A/C compressor belt, condenser inspection, cabin pressure test, measuring the vent air temperature.

CRS Automotive is an OMVIC-certified dealer, so come to Cambridge, ON, today and buy a car from us. Also, if you want to slow down the depreciation on your car, come to your trusted mechanic in Hamilton and we will take care of your car.

We are located only 4 min walking South West of Tim Hortons Field and 4 min walk West of Bernie Morelli Recreation Centre.